Succeed in BUSINESS.Succeed in LIFE.

I help entrepreneurs and business owners save $10,000 to $100,000 in taxes (legally and ethically).

MICHEL VALBRUN, CPA

TAX STRATEGIST, AWARD-WINNING AUTHOR

Your Coach for the 2017 Modern World

Helping you achieve your goals faster than you ever believed possible - that's my job.

As Featured In

As Featured In

I Can Help You Achieve Your Wildest Dreams

WHAT DO YOU WANT TO IMPROVE TODAY?

I’ve always loved business and entrepreneurship. Both my parents came from Haiti and were entrepreneurs that owned their own tax practice in Miami, Florida. The idea that I could make or create something of value for someone and have an impact on their life was exciting to me. As such, I went to the University of Florida to pursue a career in accounting so I can help as many entrepreneurs and business owners as possible.

Later in my career, I grew passionate about helping individuals achieve financial freedom. As a result, I've held several workshops and trainings to provide people the tools they need to achieve financial freedom.

After years of working for large accounting firms, I returned to my first love, entrepreneurship, and opened my own accounting firm. My mission is to bring my experience, knowledge and expertise to clients in a valuable way. I’ve teamed up with some of the greatest minds in the legal, financial planning and accounting fields to bring my clients advanced tax strategies and planning. My clients benefit from time-tested, advanced strategies that most accountants have never heard of.

I Can Help You Achieve Your Wildest Dreams

WHAT DO YOU WANT TO IMPROVE TODAY?

I’ve always loved business and entrepreneurship. Both my parents came from Haiti and were entrepreneurs that owned their own tax practice in Miami, Florida. The idea that I could make or create something of value for someone and have an impact on their life was exciting to me. As such, I went to the University of Florida to pursue a career in accounting so I can help as many entrepreneurs and business owners as possible.

Later in my career, I grew passionate about helping individuals achieve financial freedom. As a result, I've held several workshops and trainings to provide people the tools they need to achieve financial freedom.

After years of working for large accounting firms, I returned to my first love, entrepreneurship, and opened my own accounting firm. My mission is to bring my experience, knowledge and expertise to clients in a valuable way. I’ve teamed up with some of the greatest minds in the legal, financial planning and accounting fields to bring my clients advanced tax strategies and planning. My clients benefit from time-tested, advanced strategies that most accountants have never heard of.

CLAIM YOUR FREE BUSINESS SUCCESS BOOK

AVAILABLE NOW ON ALL PLATFORMS!

Imagine significantly increasing your profits to be able to achieve even more financial freedom, success, and happiness in your life. In my book, Prolific Profit.

Get Prolific Profit FREE (just pay S&H) to maximize profits and dominate in any economy.

CLAIM YOUR FREE BUSINESS SUCCESS BOOK

AVAILABLE NOW ON ALL PLATFORMS!

Imagine significantly increasing your profits to be able to achieve even more financial freedom, success, and happiness in your life. In my book, Prolific Profit.

Get Prolific Profit FREE (just pay S&H) to maximize profits and dominate in any economy.

Clarity

Understand where you are in your business and determine where you want to go

Power

5-DAY

PROLIFIC PROFIT CHALLENGE

Accountability

Work with a professional that will keep you on track and give you peace of mind

Repeat

Review your results, adjust where necessary, and repeat the process

Create a plan of action to get you on the path to achieving Prolific Profit in record time.

CLARITY

Understand where you are in your business and determine where you want to go

POWER

Gain the tools, knowledge, and information that you need to achieve your goals

Work with a professional that will keep you on track and give you peace of mind

REPEAT

Review your results, adjust where necessary, and repeat the process

Featured Testimonial

Michel has been my go-to resource regarding small business

For any of you that are small businesses owners and know the confusion that can come with running a business, it's nice to have someone to work with that can give you the answers you need so you don't have to second guess it

GianCarlo L.

Principal - Business Operations at Patina Construction & Development, LLC

Featured Testimonial

Michel has been my go-to resource regarding small business

For any of you that are small businesses owners and know the confusion that can come with running a business, it's nice to have someone to work with that can give you the answers you need so you don't have to second guess it

GianCarlo L.

Principal - Business Operations at Patina Construction & Development, LLC

Trust Me. If I Can Do It, So Can You.

Hear about my "rags to riches" story.

Hear about my "rags to riches" story.

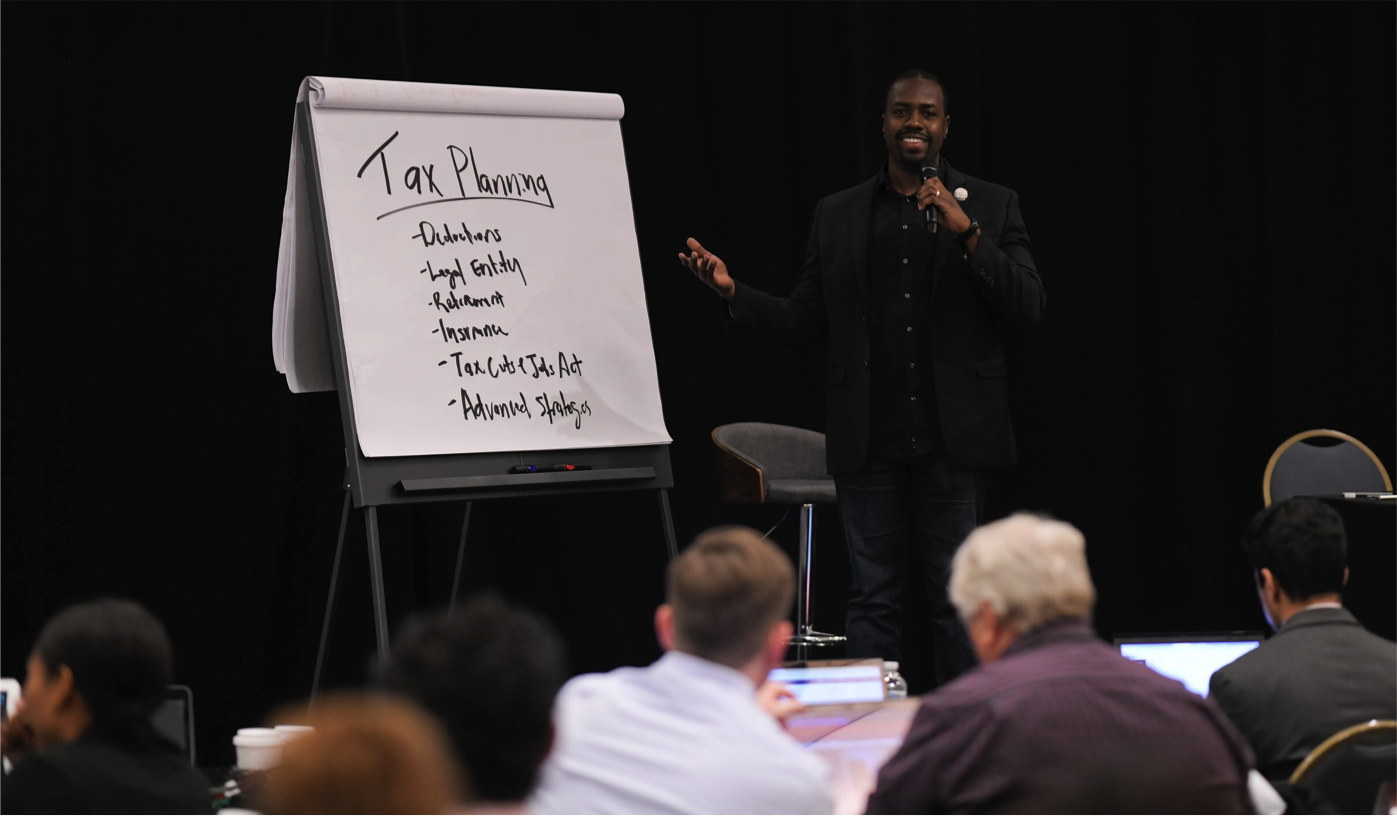

Tax Planning

Planning is the key to successfully and legally reducing your tax liability. We go beyond tax compliance and proactively recommend tax saving strategies.

Speaking

If you are looking for a blend of high energy and expertise, you have come to the right place! I would love to speak your organization.

Services I Offer

If you are willing to push harder than you ever have before: and then push a little harder; you have what it takes to earn anything you want.

CPA Services

You have more important things to do than to keep your own books. We take care of your books, so you can get back to the job of running your business.

Consulting

Increase your finances and plan for your future. We sit down together, go through your goals, and help you get on the right track with your finances.

Services I Offer

If you are willing to push harder than you ever have before: and then push a little harder; you have what it takes to earn anything you want.

Tax Planning

Planning is the key to successfully and legally reducing your tax liability. We go beyond tax compliance and proactively recommend tax saving strategies.

Speaking

If you are looking for a blend of high energy and expertise, you have come to the right place! I would love to speak your organization.

Accounting Services

You have more important things to do than to keep your own books. We take care of your books, so you can get back to the job of running your business and growing profits.

Consulting

Increase your finances and plan for your future. We sit down together, go through your goals, and help you get on the right track with your finances.

"Working with Michel has been extremely valuable..."

He provided insight and expertise for my company. If you're in the market for a tax strategist or general guidance when it comes to your business finances, I highly recommend him.

"He provided cutting edge tax solutions..."

Michel is a highly skilled tax strategist and professional. I've had the pleasure of knowing him for years. He was able to provide us with cutting edge tax solutions and save our firm more money.

CUSTOM JAVASCRIPT / HTML

"Working with Michel has been extremely valuable..."

He provided insight and expertise for my company. If you're in the market for a tax strategist or general guidance when it comes to your business finances, I highly recommend him.

"He provided cutting edge tax solutions..."

Michel is a highly skilled tax strategist and professional. I've had the pleasure of knowing him for years. He was able to provide us with cutting edge tax solutions and save our firm more money.

CUSTOM JAVASCRIPT / HTML

About Me

MICHEL VALBURN, CPA

Award-Winning Author, Tax Strategist, Speaker

Renown International Business Speaker, Michel Valbrun is Inspiring Entrepreneurs and Business Owners To Aim Higher.

Corporations, schools, and organizations bring Michel in to speak and inspire in areas concerning:

About Me

MICHEL VALBRUN, CPA

Award-Winning Author, Tax Strategist, Speaker

Renown International Business Speaker, Michel Valbrun is Inspiring Entrepreneurs and Business Owners To Aim Higher.

Corporations, schools, and organizations bring Michel in to speak and inspire in areas concerning:

- Tax Planning and Asset Protection

- Wealth Building and Legacy

- Systemizing Your Business and Cash Flow

- Personal Finance and Accounting

10 +

Years of Experience

$9MM +

Taxes Saved for Clients

27+

Speaking Events

14+

Publications

* Free Download for Entrepreneurs and Business Owners

10 +

Years of Experience

$9MM +

Taxes Saved for Clients

27 +

Speaking Events

14 +

Publication Features

PROLIFIC PROFIT © 2020. All Rights Reserved